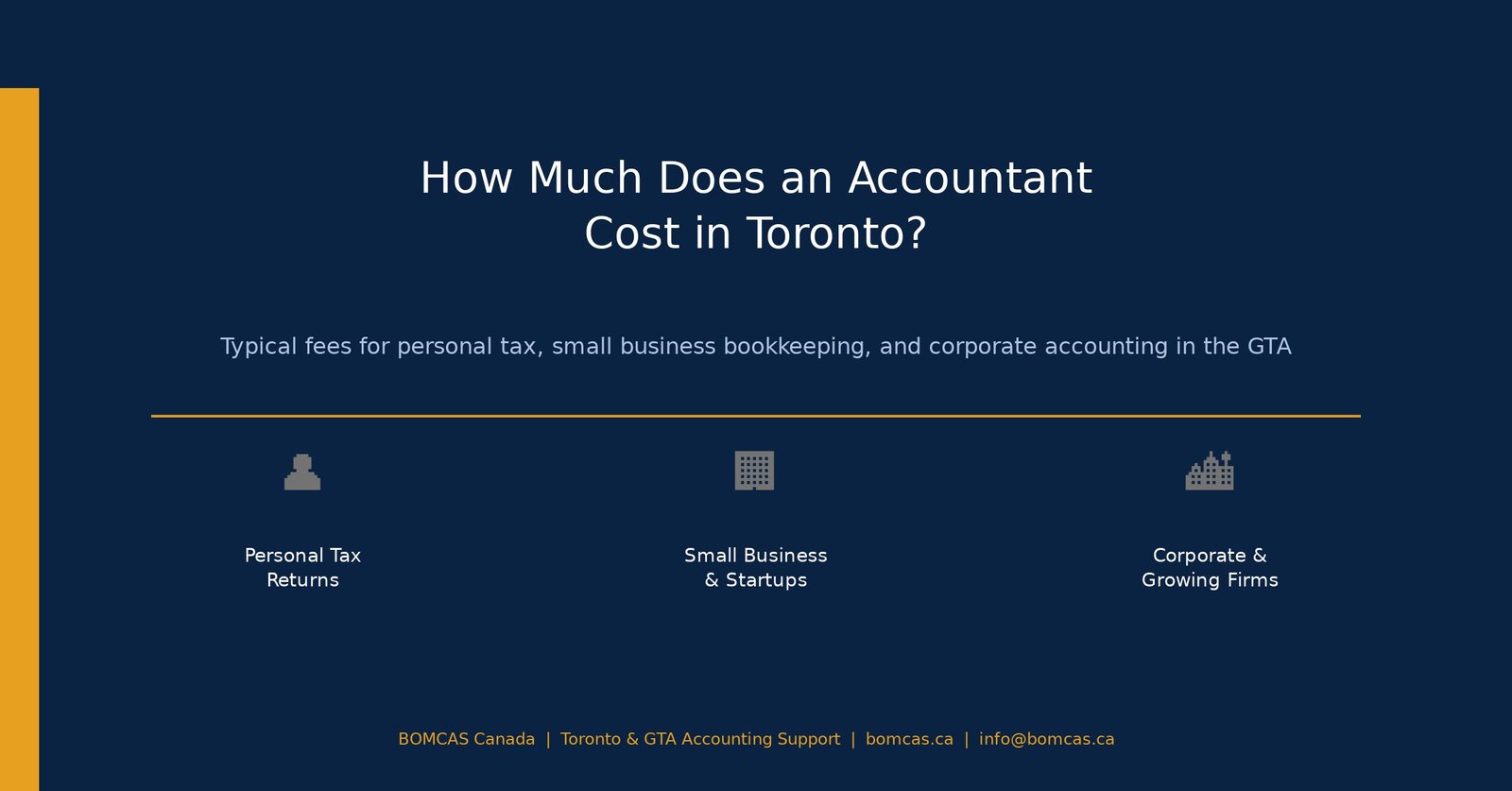

How much does an accountant cost in Toronto?

In Toronto, accountant costs typically range from about 150 to 400 dollars per hour...

Canada's Top Professionals

Canada's Top Professionals

Need Help? Call Us At

780-667-5250Providing Accounting & Tax service in Canada.

Non-resident individuals are only obligated to pay income taxes on the earnings they generate while physically present in the country when it comes to income taxes in Jamaica. Residents and incorporated individuals are required to pay income taxes on their worldwide profits, whereas residents and incorporated individuals are only required to pay income taxes on the earnings they generate while physically present in the country. It is generally accepted that when income is generated from foreign sources, non-Jamaicans are exempt from paying tax on such income until that revenue is transferred back to the nation of origin. Workers in Jamaica who are not residents of the country are subject to taxation on both compensation for services rendered within and in relation to the country (with limited exclusions) and income earned within the country, regardless of where they are domiciled in the world. Workers in Jamaica who are not residents of the country are subject to taxation on compensation for services rendered within and in relation to the country (with limited exclusions).

Personal income tax is levied at a 25% rate on chargeable income (which cannot exceed JMD 6 million per year) less a tax-free threshold of JMD 500,000 per year (where applicable). In the case of chargeable income in excess of JMD 6 million per year, the amount is subject to income tax at a 30% rate. Individuals who are tax residents of Jamaica are entitled to a tax-free income threshold of JMD 1.5 million per year.

Individuals are subjected to taxation at the national level. At the local level, there is no separate imposition of income tax.

In Toronto, accountant costs typically range from about 150 to 400 dollars per hour...

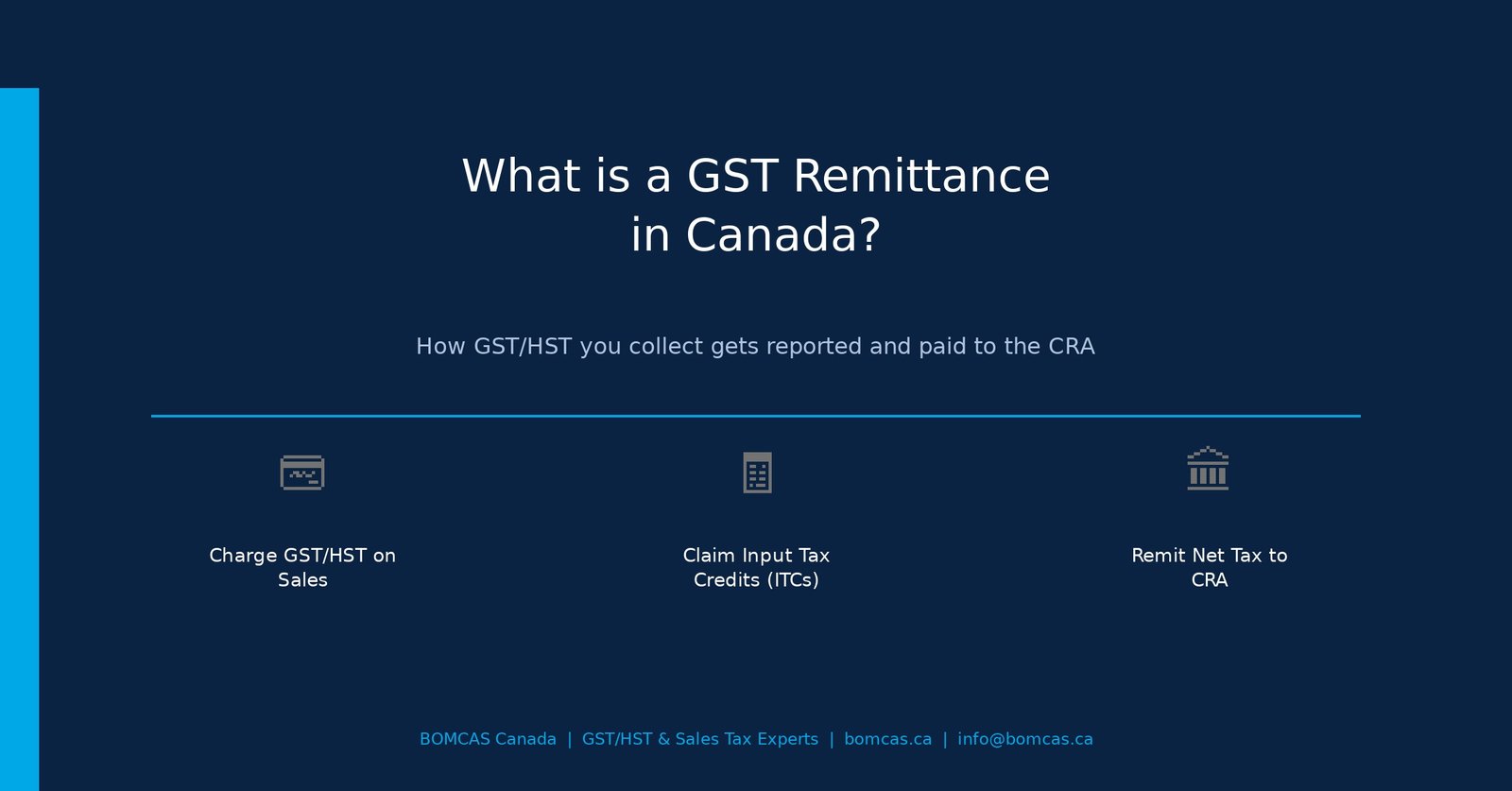

A GST remittance in Canada is the process of reporting and paying to the...

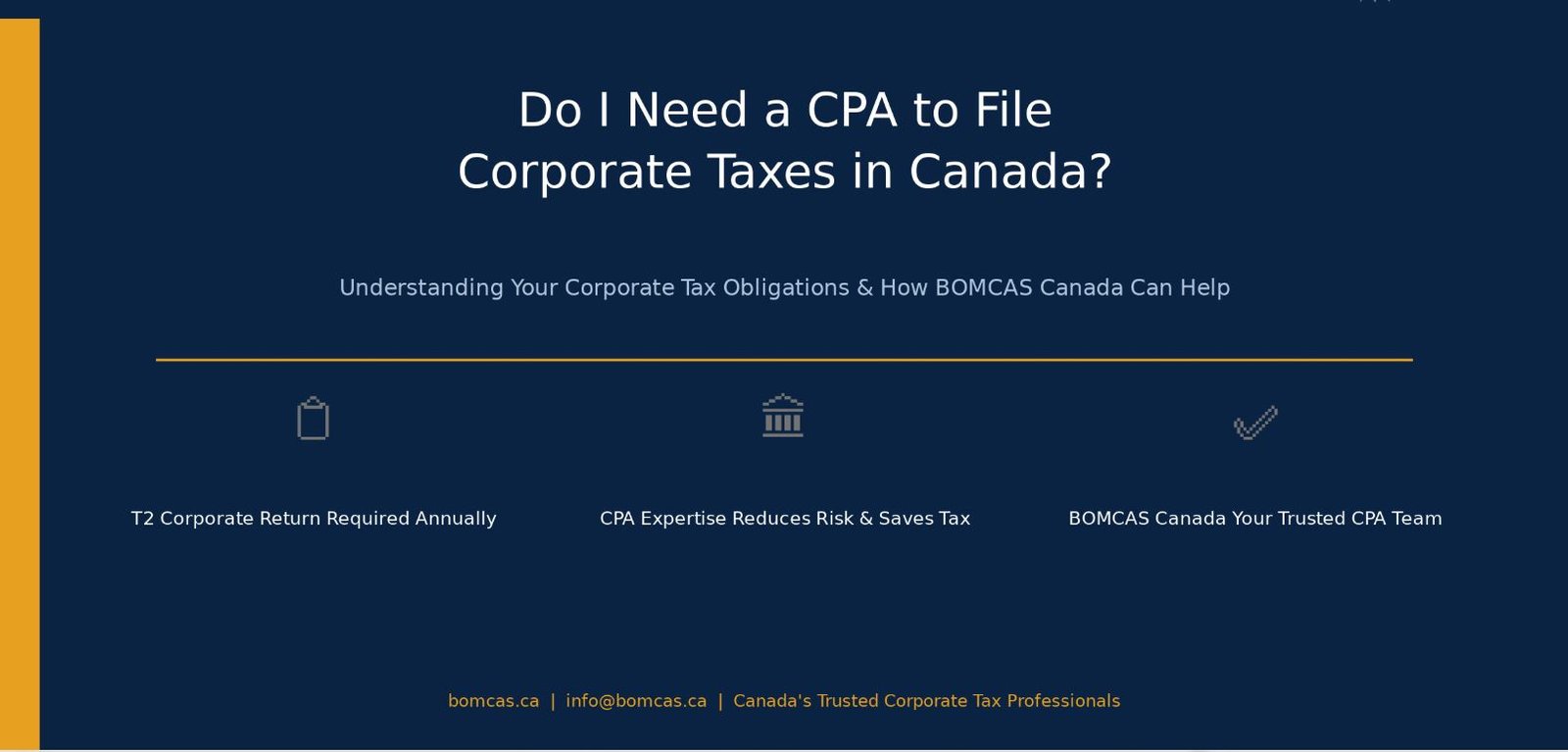

If you own a corporation in Canada, one of the most pressing questions you'll...

Ontario business owners face a complex mix of federal and provincial tax rules, but...

Ontario business owners have many opportunities to reduce taxable income through legitimate tax write-offs....

Small business owners in Ontario can reduce taxable income significantly by claiming all legitimate...

There is no single income number or universal rule that tells every Canadian business...

For Canadian entrepreneurs, choosing between operating as a sole proprietor or incorporating a company...

181 Meadowview Bay, Sherwood Park, AB T8H 1P7, Canada (Online Clients Only)

181 Meadowview Bay, Sherwood Park, AB T8H 1P7, Canada (Online Clients Only)

6063 88 St NW, Edmonton, AB T6E 5T4, Canada

Calgary, Alberta, Canada (Coming Soon)

View Our Location

View Our Location