Executive Summary

Canada’s Goods and Services Tax (GST) and Harmonized Sales Tax (HST) system is one of the most complex parts of business compliance—yet most Canadian business owners don’t understand the critical differences between quarterly and annual filing, provincial variations, or the penalties for missing deadlines. The result: thousands of businesses pay late, miss remittance windows, or file on the wrong forms, costing them thousands in interest and penalties.

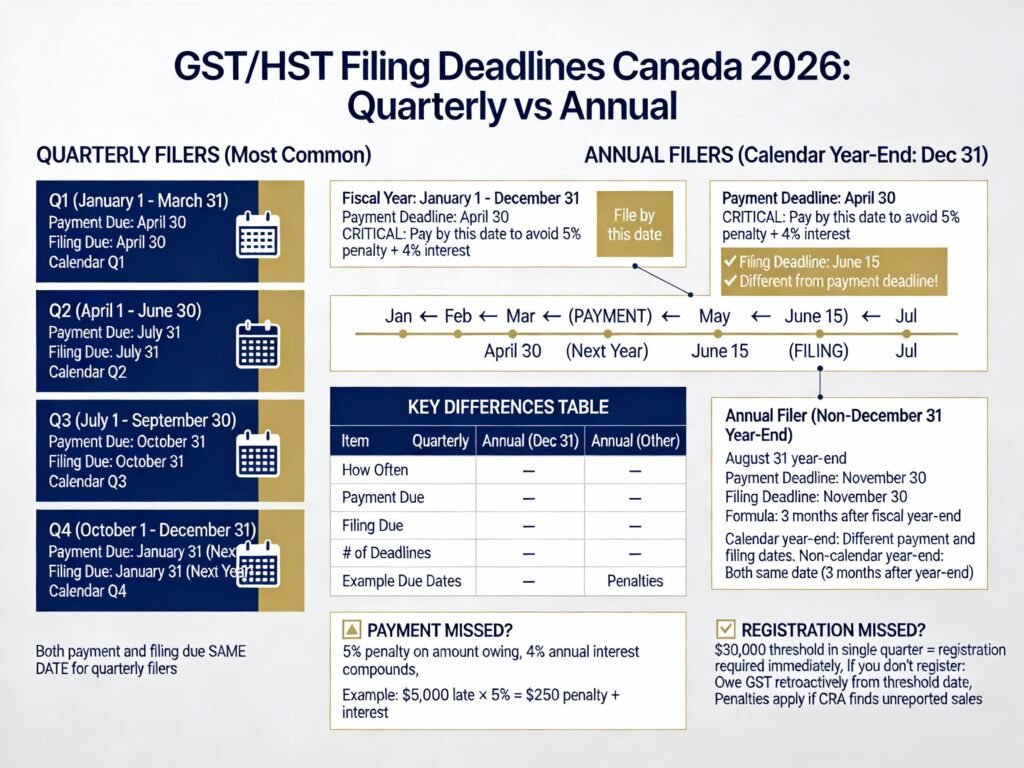

The stakes are significant. Missing a GST/HST filing deadline can cost 5% penalty on late payment, plus 4% annual interest. Missing a registration deadline when your revenue exceeds $30,000 can trigger a retroactive assessment covering months or years of uncollected tax—which you must pay from your own pocket.

This guide explains every aspect of Canadian GST/HST filing: when you must register, whether to file quarterly or annually, exact payment deadlines for all provinces, input tax credit (ITC) strategies to maximize refunds, provincial variations (Alberta vs Ontario vs Quebec), and step-by-step filing instructions for 2026.

For Canadian business owners, understanding GST/HST filing deadlines and requirements is the difference between compliant operations and costly penalties.

Part 1: When Must You Register for GST/HST?

The $30,000 Threshold (Federal Rule)

The Critical Threshold Rule:

You MUST register for GST/HST if your business revenue exceeds:

- $30,000 in any single calendar quarter (three consecutive months), OR

- $30,000 within any four consecutive calendar quarters (not calendar year)

Important: This threshold is based on REVENUE, not profit.

What Counts Toward the Threshold:

- Taxable supplies (normal business sales)

- Zero-rated supplies (still count toward threshold)

- Worldwide revenue (from all countries)

- Related business revenue (if you own multiple businesses)

- Personal + corporate revenue (if linked)

What Does NOT Count:

- Exempt supplies (health, education, childcare, financial services)

- Employment income (wages as employee)

- Personal income not from business

Example of Threshold Trigger:

- Q1: $9,000 revenue

- Q2: $8,000 revenue

- Q3: $7,500 revenue

- Q4: $7,800 revenue

- Total: $32,300 → Registration required immediately

Single Quarter Trigger:

- Q1: $31,500 revenue

- Threshold exceeded in that quarter → Registration required immediately

Who Must Register Before $30,000?

You are NOT required to register if you:

- Remain below $30,000 threshold AND

- Provide exclusively exempt services (some health, education, childcare, finance)

Who Can Voluntarily Register Before $30,000?

Voluntary registration is beneficial if:

- Your clients are primarily businesses (B2B)

- You have significant startup expenses

- You want to claim input tax credits (ITCs) immediately

- You expect rapid growth

- You want professional invoices with GST/HST

Benefit of Voluntary Registration:

You can immediately claim ITCs on business expenses, creating potentially significant refunds.

Registration Consequences When You Miss the Threshold

If you exceed $30,000 without registering:

- You MUST register immediately

- You owe GST/HST on all sales retroactively

- You cannot claim ITCs on expenses until registered

- You may face penalties (5% on late payment minimum)

- You may face interest charges (4% annually)

- You may be subject to audit

- Clients may refuse to pay retroactive tax

Part 2: GST vs. HST vs. PST: Provincial Breakdown

What Are the Differences?

GST (Goods and Services Tax):

- Federal tax only: 5%

- Administered by Canada Revenue Agency (CRA)

- Applies in: Alberta, BC, Manitoba, Saskatchewan, Yukon, NWT, Nunavut, Quebec (5% only)

- Combined with provincial sales tax (PST) or Quebec Sales Tax (QST)

HST (Harmonized Sales Tax):

- Federal + provincial combined into single tax

- Administered by CRA (except Quebec)

- Applies in: Ontario (13%), New Brunswick (15%), Newfoundland & Labrador (15%), Nova Scotia (14%), PEI (15%)

- Simplified filing (one rate, one form)

PST (Provincial Sales Tax):

- Provincial tax only (no federal component in PST filing)

- Applied on top of 5% GST

- Applies in: BC (7%), Manitoba (7%), Saskatchewan (6%)

- Requires separate registration and filing

QST (Quebec Sales Tax):

- Quebec’s equivalent to HST

- Administered by Revenu Québec (not CRA)

- Rate: 9.975% (in addition to 5% GST)

- Separate system from federal GST

Provincial Tax Rates (2026)

| Province | Type | Federal | Provincial | Total |

|---|---|---|---|---|

| Alberta | GST | 5% | 0% | 5% |

| BC | GST + PST | 5% | 7% | 12% |

| Manitoba | GST + PST | 5% | 7% | 12% |

| Saskatchewan | GST + PST | 5% | 6% | 11% |

| Ontario | HST | — | — | 13% |

| New Brunswick | HST | — | — | 15% |

| Newfoundland | HST | — | — | 15% |

| Nova Scotia | HST | — | — | 14% |

| PEI | HST | — | — | 15% |

| Quebec | GST + QST | 5% | 9.975% | 14.975% |

| Yukon | GST | 5% | 0% | 5% |

| NWT | GST | 5% | 0% | 5% |

| Nunavut | GST | 5% | 0% | 5% |

Part 3: Filing Frequency: Monthly, Quarterly, or Annual?

How Is Filing Frequency Determined?

The CRA determines your filing frequency based on:

- Your annual revenues

- Your business type

- Your preferences

- Compliance history

Most Common: Quarterly or Annual

Filing Frequency Options

Monthly Filing

Who Files Monthly:

- Larger businesses with higher revenues

- Businesses that prefer frequent cash flow management

- Businesses in specific industries

- Generally voluntary (not mandatory)

Deadline:

- Due one month after end of reporting period

- Example: July 1–31 reporting period → Due August 31

Payment:

- Same as filing deadline (one month after period ends)

Quarterly Filing

Most Common: Quarterly filing for small-to-medium businesses

Reporting Periods (Calendar Quarters):

- Q1: January 1–March 31 → Due April 30

- Q2: April 1–June 30 → Due July 31

- Q3: July 1–September 30 → Due October 31

- Q4: October 1–December 31 → Due January 31

Payment:

- Same as filing deadline

Note: Some businesses have fiscal quarters (not calendar quarters). Your CRA notice of assessment specifies your exact reporting periods.

Annual Filing

Most Common: For smaller businesses, sole proprietors, incorporated companies

Reporting Period:

- Calendar year: January 1–December 31

- OR fiscal year (custom year-end)

Payment and Filing Deadlines (Calendar Year-End):

- Filing deadline: June 15

- Payment deadline: April 30

- Sole proprietors: Aligned with income tax deadline

Example (Fiscal Year-End August 31):

- Reporting period: September 1, 2024–August 31, 2025

- Payment deadline: November 30, 2025

- Filing deadline: November 30, 2025

Important Note: For annual filers with calendar year-end:

- You MUST file by June 15

- You MUST pay by April 30

- Filing and payment have different deadlines

Part 4: GST/HST Payment Deadlines by Province (2026)

Quarterly Filers

| Reporting Period | Payment Deadline | Filing Deadline |

|---|---|---|

| Jan 1–Mar 31 | April 30 | April 30 |

| Apr 1–Jun 30 | July 31 | July 31 |

| Jul 1–Sep 30 | October 31 | October 31 |

| Oct 1–Dec 31 | January 31 (next year) | January 31 (next year) |

Annual Filers with December 31 Year-End

| Deadline | Date |

|---|---|

| Payment Deadline | April 30 |

| Filing Deadline | June 15 |

| Business Days After Period Ends | ~4 months payment, ~5.5 months filing |

Annual Filers with Non-December 31 Year-End

| Item | Deadline |

|---|---|

| Payment Deadline | 3 months after fiscal year-end |

| Filing Deadline | 3 months after fiscal year-end |

Example (August 31 Year-End):

- Year-end: August 31

- Payment deadline: November 30

- Filing deadline: November 30

Sole Proprietors and Partners

If you are self-employed or a partner:

- Your GST/HST return aligns with personal income tax deadline

- Payment deadline: April 30 (for calendar year)

- Filing deadline: June 15 (for calendar year)

- Combined with personal T1 return filing

Part 5: Quarterly Instalment Payments (If You Owe $3,000+)

Who Must Make Quarterly Instalments?

If you owed $3,000 or more in GST/HST in the previous year (or current year), you may be required to make quarterly instalment payments, even if you file annually.

This is different from filing quarterly:

- You can be an annual filer (file once per year) BUT

- Make quarterly payments (pay four times per year)

Instalment Payment Dates

| Period | Due Date |

|---|---|

| Q1 (Jan–Mar) | April 30 |

| Q2 (Apr–Jun) | July 31 |

| Q3 (Jul–Sep) | October 31 |

| Q4 (Oct–Dec) | January 31 (next year) |

How Instalments Work

- Calculate: Last year’s GST/HST owing ÷ 4

- Pay that amount each quarter

- File one annual return showing total owing for year

- Final payment/refund reconciled in annual return

Part 6: Ontario (13% HST) – Specific Requirements

Ontario HST Rate

- 13% HST (combined federal + provincial)

- Single tax code, single registration, single form

- Administered by CRA

Ontario Filing Requirements (Same as Federal)

Quarterly Filers:

- Q1 (Jan–Mar): Due April 30

- Q2 (Apr–Jun): Due July 31

- Q3 (Jul–Sep): Due October 31

- Q4 (Oct–Dec): Due January 31

Annual Filers (Dec 31 year-end):

- Payment: April 30

- Filing: June 15

Ontario Special Notes

- No separate provincial registration needed

- One HST number covers federal + provincial

- Input tax credits are claimed on federal form (line 106)

Part 7: Quebec (5% GST + 9.975% QST) – Special Requirements

Quebec’s Two-Tier System

Federal GST: 5%

- Administered by CRA

- Filed with federal form

Quebec QST (Sales Tax): 9.975%

- Administered by Revenu Québec (not CRA)

- Filed with separate provincial form

- Similar rules to GST but separate system

Total combined: 14.975%

Quebec Registration Requirements

QST Registration Threshold: Same as GST ($30,000)

- Registration mandatory when revenue exceeds $30,000

- Threshold calculated same way (one quarter or four consecutive quarters)

Outside-Quebec Businesses Selling to Quebec:

- If you make sales to Quebec customers, you may be required to register for QST

- If sales to Quebec exceed $30,000, registration is mandatory

- Must charge QST on sales to Quebec residents

Quebec Filing with Revenu Québec

If your business is physically located in Quebec:

- File GST with CRA

- File QST with Revenu Québec

- Two separate registrations

- Two separate returns

Special Financial Institutions Exemption:

- SLFIs (Selected Listed Financial Institutions) may file combined returns

- Most regular businesses file separately

Quebec Filing Deadlines

GST (with CRA): Standard federal deadlines (same as Ontario)

QST (with Revenu Québec): Similar schedule but administered separately

Part 8: Alberta (5% GST Only) – Simplest System

Alberta GST Rate

- 5% GST only (no provincial sales tax)

- No PST, no additional provincial tax

- Lowest combined tax rate in Canada

Alberta Registration and Filing

- GST registration same as federal ($30,000 threshold)

- One registration, one form

- Administered by CRA

- Same deadlines as Ontario

Alberta Filing Deadlines

Quarterly:

- April 30, July 31, October 31, January 31

Annual (Dec 31 year-end):

- Payment: April 30

- Filing: June 15

Part 9: Input Tax Credits (ITCs)—Maximize Tax Recovery

What Are Input Tax Credits?

Input Tax Credits allow you to recover (claim back) the GST/HST you paid on business expenses and purchases.

Basic Rule: You can claim ITCs for GST/HST paid on expenses used in your commercial activities.

Eligible Expenses for ITCs

Operating Expenses:

- Rent (commercial space)

- Utilities (electricity, water, internet)

- Office equipment and supplies

- Accounting and legal professional fees

- Advertising and marketing

- Insurance (business)

- Maintenance and repairs

- Motor vehicle expenses

- Travel (hotels, flights, car rentals)

- Meals and entertainment (certain % only)

Capital Expenses:

- Machinery and equipment

- Vehicles and automotive equipment

- Furniture and appliances

- Property improvements

- Depreciable property

Non-Eligible Expenses (NO ITCs)

- Personal consumption items

- Recreation club membership fees (golf, fitness clubs)

- Certain capital property restrictions

- Expenses for exempt supplies

- Personal use (home office mixed use)

- Meals and entertainment (partial only)

How to Calculate ITCs

Basic Formula:

textGST/HST paid on expense = ITC amount

Example:

- Rent: $1,000 + 5% GST = $1,050 paid

- ITC: $50 recoverable

- Report on GST/HST return line 106

Mixed Use Expenses:

- If expense partly business, partly personal

- Only claim ITC for business-use portion

- Example: Home office 30% business use = claim 30% of GST/HST

Timing of ITC Claims

- Claim in filing period when you paid the tax

- Must have GST/HST registration number

- Must be registered to claim ITCs

- Support documentation required

Part 10: Filing Your GST/HST Return

Electronic Filing Requirement

As of January 1, 2024: Electronic filing is MANDATORY for all GST/HST registrants except:

- Selected listed financial institutions (SLFIs)

- Certain charities

- Deceased taxpayers

- Non-residents (limited exceptions)

Filing Methods:

- CRA NETFILE (online)

- Accounting software

- Tax professional (accountant, bookkeeper)

What Information to Report

On Your GST/HST Return, Report:

- Gross revenue (all sales)

- Taxable sales (at applicable GST/HST rate)

- Zero-rated sales (count as revenue but no tax)

- Exempt sales (health, education, etc.)

- GST/HST collected (sales tax you charged customers)

- Input tax credits (GST/HST you paid on expenses)

- Net remittance (GST/HST collected minus ITCs)

GST/HST Return Calculation

textGST/HST Collected (sales tax charged to customers)

Minus: Input Tax Credits (tax paid on purchases)

= Net GST/HST Remittance (amount you owe CRA or refund due)

Part 11: Common GST/HST Filing Mistakes

Mistake #1: Forgetting to Register at $30,000

Problem:

- Exceed $30,000 threshold without registering

- Continue invoicing customers without tax

Consequence:

- Retroactive registration from threshold date

- Owe GST/HST on all sales

- Personal tax liability (you must pay)

- Penalties and interest

Prevention:

- Monitor revenue quarterly

- Register before or at $30,000

- Use accounting software to track

Mistake #2: Confusing Filing and Payment Deadlines

Problem:

- Annual filers: Payment due April 30, filing due June 15

- Paying on June 15 (filing date) costs penalty on late payment

Consequence:

- 5% late payment penalty

- 4% annual interest

- Costs compound over time

Prevention:

- Mark calendar: April 30 payment date

- Mark calendar: June 15 filing date

- Pay by April 30 to avoid penalty

Mistake #3: Not Claiming All Eligible ITCs

Problem:

- Forgetting to track business expenses

- Not claiming GST/HST paid on purchases

- Overpaying GST/HST owing

Consequence:

- Overpaying taxes (money left on table)

- Losing refunds

- Cashflow problem

Prevention:

- Keep all receipts

- Track expenses in software

- Claim all eligible ITCs

Mistake #4: Mixing Personal and Business Expenses

Problem:

- Claiming ITCs on personal consumption items

- Claiming home office at 100% when only 30% business use

Consequence:

- Audit risk

- Required to repay ITCs claimed

- Penalties

Prevention:

- Allocate mixed expenses (% business use)

- Keep business and personal separate

- Document business purpose

Part 12: Examples and Calculations

Example 1: Quarterly Filer (Ontario, 13% HST)

Scenario:

- Business in Toronto

- Quarterly filer

- Q1 reporting period: Jan 1–Mar 31

Numbers:

- Gross sales: $50,000

- HST collected from customers: $6,500 (13%)

- Expenses: $20,000

- HST paid on expenses: $2,600 (13%)

- Input tax credits: $2,600

Calculation:

- HST collected: $6,500

- Minus: ITCs: $2,600

- Net HST owing: $3,900

Deadline:

- Due: April 30, 2026

Example 2: Annual Filer (Alberta, 5% GST)

Scenario:

- Business in Calgary

- Annual filer

- Fiscal year: Jan 1–Dec 31

Numbers:

- Gross sales: $200,000

- GST collected: $10,000 (5%)

- Expenses: $100,000

- GST paid on expenses: $5,000 (5%)

- ITCs: $5,000

Calculation:

- GST collected: $10,000

- Minus: ITCs: $5,000

- Net GST owing: $5,000

Deadlines:

- Payment due: April 30, 2026

- Filing due: June 15, 2026

Example 3: Exceeding $30,000 Threshold

Scenario:

- Freelance consultant, no GST registration

- Revenue tracking:

- Q1: $8,000

- Q2: $9,000

- Q3: $8,500

- Q4: $6,000

- Total: $31,500

Status:

- Exceeded $30,000 in Q3

- Registration becomes mandatory immediately (not at year-end)

- Must start charging GST on next invoice

Consequence:

- Retroactive registration to Q3 date

- If didn’t register: Owe GST on all sales back to Q3

- Penalty: 5% on late payment + 4% interest

Part 13: Key Dates for 2026

| Date | Event |

|---|---|

| January 31 | Q4 (Oct–Dec) quarterly return due |

| February 28 | Monthly filer deadline (January returns) |

| April 30 | Q1 (Jan–Mar) quarterly return due; Annual filer payment due |

| May 31 | Monthly filer deadline (April returns) |

| June 15 | Annual filer (Dec 31 year-end) filing due; Self-employed deadline |

| June 30 | Monthly filer deadline (May returns) |

| July 31 | Q2 (Apr–Jun) quarterly return due; Monthly filer (June) due |

| August 31 | Monthly filer deadline (July returns) |

| October 31 | Q3 (Jul–Sep) quarterly return due; Monthly filer (September) due |

| November 30 | Monthly filer deadline (October returns) |

Conclusion: GST/HST Compliance is Essential

For Canadian business owners, understanding GST/HST filing deadlines, provincial variations, and ITC strategies is critical to maintaining compliance and avoiding costly penalties. Missing a $30,000 registration deadline can cost thousands in retroactive tax. Missing a payment deadline costs 5% penalty plus 4% interest. Missing ITCs costs cashflow.

The good news: Modern accounting software makes GST/HST compliance straightforward. Tracking expenses, claiming ITCs, and filing on deadline is achievable with proper systems.

Your action plan:

- Determine your revenue against $30,000 threshold

- Register if exceeded

- Understand your filing frequency (monthly, quarterly, annual)

- Mark payment and filing deadlines in your calendar

- Track all eligible expenses for ITCs

- File electronically by deadline

- Claim all eligible ITCs

Article created for BOMCAS Canada. For GST/HST filing help and compliance services, contact info@bomcas.ca

View Our Location

View Our Location

181 Meadowview Bay, Sherwood Park, AB T8H 1P7, Canada (Online Clients Only)

181 Meadowview Bay, Sherwood Park, AB T8H 1P7, Canada (Online Clients Only)