Executive Summary

For Canadian small business owners and self-employed professionals, understanding tax deductions and credits is the difference between keeping maximum after-tax profit and leaving money on the table. Yet many business owners claim only 50-70% of eligible deductions, leaving thousands in unclaimed tax savings annually.

The challenge is complexity: The Canada Revenue Agency (CRA) allows dozens of deduction categories, each with specific eligibility rules, documentation requirements, and calculation methods. Home office expenses have different rules depending on whether you’re self-employed or an employee. Vehicle expenses require detailed mileage tracking. Meal and entertainment expenses are subject to the 50% rule—but with multiple exceptions.

For Canadian-controlled private corporations (CCPCs), tax credits—not just deductions—can provide even more substantial savings. The Small Business Deduction (SBD) reduces federal tax from 15% to 9% on the first $500,000 of active business income, saving $30,000 annually. The Scientific Research & Experimental Development (SR&ED) program provides up to 35% tax credits on R&D spending, effectively reducing innovation costs by over one-third.

This comprehensive 2026 guide outlines every major deduction category available to Canadian small businesses, provides real calculation examples, explains tax credits, and offers checklists to ensure you claim every eligible expense—legally and with full CRA compliance.

Part 1: The Big Four Deductions (Largest Tax Savings Opportunities)

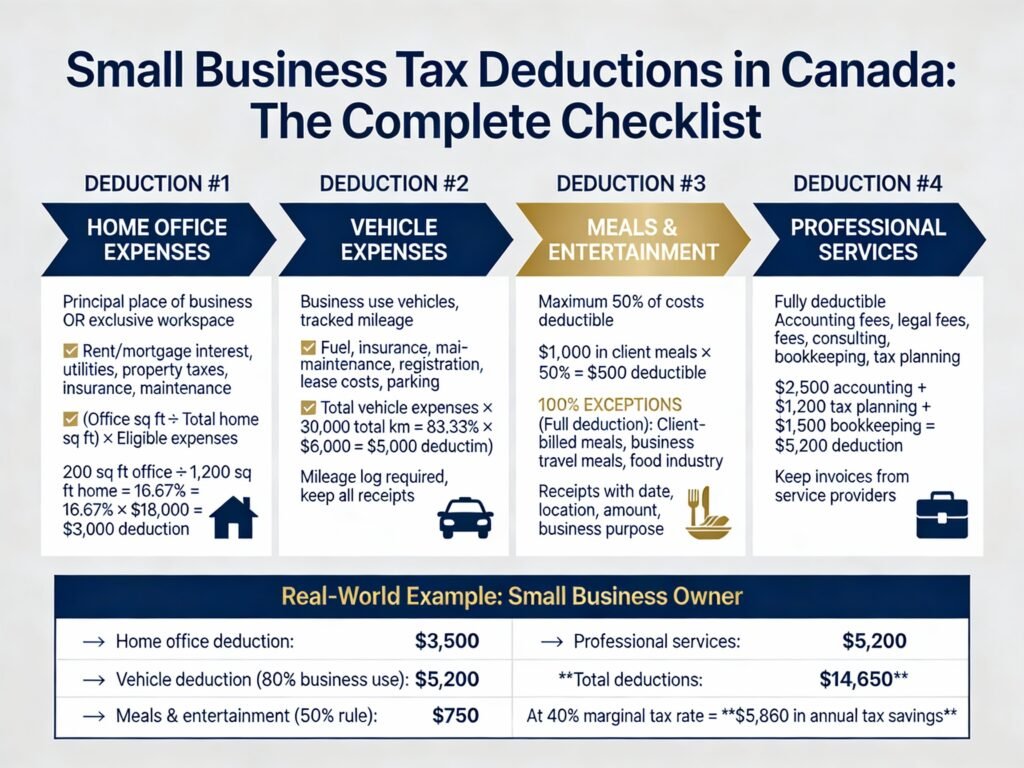

Deduction #1: Home Office Expenses (Up to $3,000-$5,000+ Annually)

Who Qualifies:

You can claim home office deductions if at least one of these applies:

- Your home is the principal place of your business

- You have a designated workspace used exclusively for business on a consistent basis

- You meet clients or customers at your home regularly (self-employed only)

Calculation Method:

Home office deduction = (Office square footage ÷ Total home square footage) × Total eligible home expenses

Example:

- Office size: 200 sq. ft.

- Total home size: 1,200 sq. ft.

- Percentage: 200 ÷ 1,200 = 16.67%

- Total annual home expenses: $18,000

- Home office deduction: $18,000 × 16.67% = $3,000

Eligible Home Office Expenses:

- Rent (or mortgage interest—NOT principal)

- Utilities: electricity, gas, water, heating, cooling

- Property taxes (self-employed only; employees cannot claim)

- Home insurance

- Maintenance and repairs

- Internet and telephone

- Property insurance

Critical Rule—Mortgage Interest vs. Principal:

- Interest = Deductible

- Principal = NOT deductible

- Example: If mortgage payment is $2,000/month ($1,200 interest, $800 principal), only the $1,200 interest can be claimed

Important Limitation for Employees:

- Employer must REQUIRE home office (not optional)

- Employer must NOT reimburse you

- You must complete and have employer sign Form T2200

- Self-employed have more flexibility (no T2200 required)

Deduction #2: Vehicle Expenses (Up to $5,000-$10,000+ Annually)

The Critical Calculation:

Vehicle deduction = Total vehicle expenses × (Business km ÷ Total km)

Example:

- Business km driven: 25,000

- Personal km driven: 5,000

- Total km: 30,000

- Business use percentage: 25,000 ÷ 30,000 = 83.33%

- Total vehicle expenses: $6,000

- Deductible vehicle expenses: $6,000 × 83.33% = $5,000

Eligible Vehicle Expenses (100% if purely business use):

- Fuel (gas, diesel, propane)

- Oil and lubricants

- Insurance

- Maintenance and repairs

- License and registration fees

- Lease costs (subject to limits)

- Interest on vehicle loan (subject to limits)

- Parking fees (full 100% deduction, not prorated)

- Electricity for zero-emission vehicles

Special Parking Rule:

Business parking fees are 100% deductible (not prorated by business %), even if the vehicle is used partly for personal purposes.

Interest Limitation on Passenger Vehicles:

- Passenger vehicle = Cap at $37,000 + GST/HST maximum cost

- If vehicle costs $50,000, only $37,000 can be depreciated

- Interest deduction also limited: Maximum $11.66 per day × number of days interest paid

- Commercial vehicles have higher limits

Documentation Required (Critical for CRA Compliance):

You must keep:

- Detailed mileage log (date, odometer start, odometer end, destination, business purpose)

- All receipts for vehicle expenses

- Two logging methods acceptable:

- Full logbook method: Track every trip all year

- Simplified logbook method: Track one full year to establish base, then track 3-month sample in subsequent years (acceptable if within 10% of base year)

Common Mistake:

Claiming commuting as business use. Your home-to-office drive is personal use, not business use, and cannot be deducted.

Deduction #3: Meals and Entertainment Expenses (50% Deductible with Exceptions)

The 50% Rule:

Maximum deductible = 50% of the LESSER of:

- Amount actually spent

- Amount reasonable in the circumstances

What’s Subject to 50% Limitation:

- Meals and beverages (includes tips, taxes)

- Entertainment tickets

- Sporting event tickets

- Gratuities and cover charges

- Room rentals for hospitality suites

Example:

- Client lunch bill: $100 (includes food, drink, tip, tax)

- 50% deductible: $100 × 50% = $50 deductible

- $50 cannot be claimed

100% Deduction Exceptions (Full Amount Deductible):

- Meals billed to client/customer: If you bill the client and add the meal cost to their invoice, claim 100%

- Food/hospitality industry: If your business is a restaurant, catering company, or hotel, claim 100% on meals/entertainment as part of business operations

- Business travel: If traveling primarily for business, meals during the trip are 100% deductible (not 50%)

- Incidental refreshments at events: Coffee, juice, muffins, and donuts at conventions/seminars are 100% deductible

- Employee cafeteria: Meals available equally to all employees in company cafeteria are 100% deductible

Documentation Requirement:

Keep receipts showing:

- Date of meal/entertainment

- Location/establishment

- Amount spent

- Business purpose

- Attendees and their relationship to business

Deduction #4: Professional Services Fees (100% Deductible)

Fully Deductible Professional Expenses:

- Accounting and bookkeeping fees

- Legal fees (business matters)

- Tax preparation and planning

- Consulting fees (business consultation)

- Financial advising

- Business advisory services

Documentation:

- Keep invoices from service providers

- Note business purpose clearly

- Ensure fees are reasonable for the service

Example:

- Annual accounting fee: $2,500 (fully deductible)

- Tax planning consultation: $1,200 (fully deductible)

- Bookkeeping services: $1,500 (fully deductible)

- Total deduction: $5,200

Part 2: Complete List of Deductible Business Expenses

Office Supplies and Equipment

- Pens, pencils, paper, ink cartridges: Fully deductible

- Office furniture under $500: Fully deductible

- Software subscriptions: Fully deductible

- Computer software under $500: Fully deductible

- Equipment over $500: Claimed via Capital Cost Allowance (CCA) depreciation

Advertising and Marketing

- Digital advertising (Google Ads, Facebook, LinkedIn): Fully deductible

- Website design and hosting: Fully deductible

- Branding and logo development: Fully deductible

- Canadian newspaper, TV, radio advertising: Fully deductible

- Social media marketing: Fully deductible

- Email marketing software: Fully deductible

- Billboards and signage: Fully deductible

Insurance

- Business liability insurance: Fully deductible

- Property insurance (building, equipment): Fully deductible

- Professional liability insurance: Fully deductible

- Commercial vehicle insurance: Fully deductible

- Workers compensation insurance: Fully deductible

Rent and Facility Expenses

- Office rent: Fully deductible

- Warehouse/storage rent: Fully deductible

- Parking (business vehicles): Fully deductible

- Utilities (if not home-based): Fully deductible

- Maintenance and repairs: Fully deductible

- Equipment rental: Fully deductible

Salaries and Employee Benefits

- Employee wages and salaries: Fully deductible

- CPP/EI contributions (employer portion): Fully deductible

- Workers compensation: Fully deductible

- Private health service plan (PHSP) premiums: Fully deductible

- Training and professional development: Fully deductible

- Employee bonuses: Fully deductible

Other Deductible Expenses

- Bad debt write-off (if previously claimed as income): Fully deductible

- Business licenses and permits: Fully deductible

- Membership dues in professional organizations: Fully deductible

- Bank fees and interest charges: Fully deductible

- Subscriptions to business publications: Fully deductible

- Shipping and delivery costs: Fully deductible

- Travel accommodation (business travel): Fully deductible

Part 3: Tax Credits for Corporations (Not Deductions—Even Better)

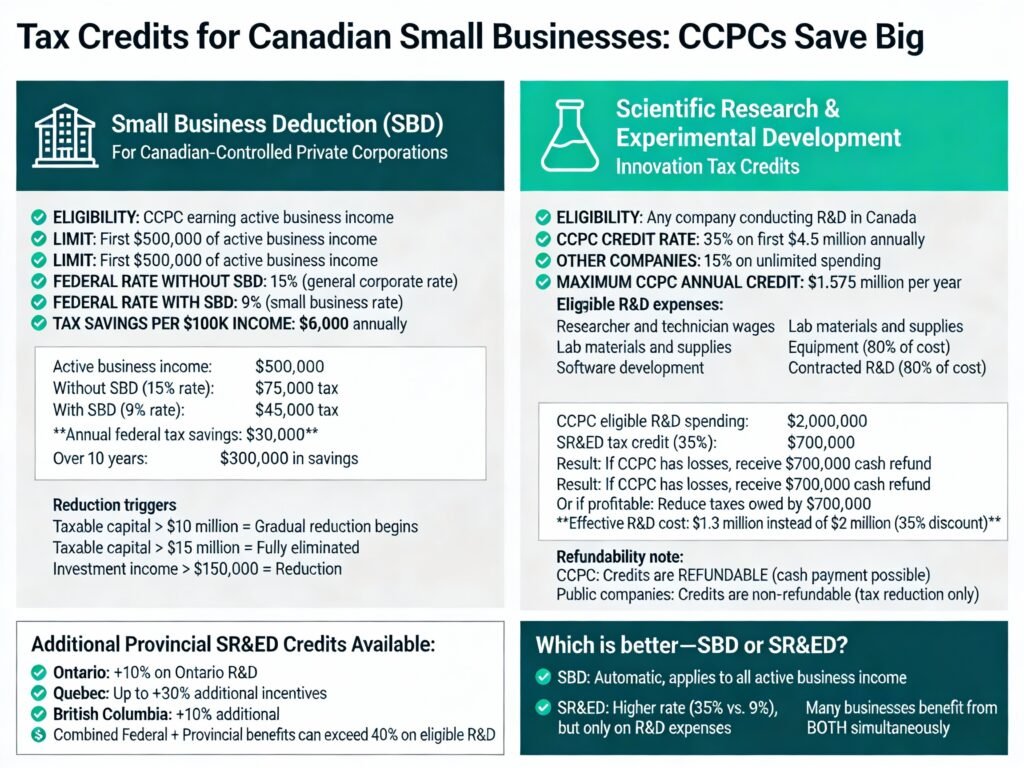

Tax Credit #1: Small Business Deduction (SBD)

What It Is:

A federal tax credit for Canadian-controlled private corporations (CCPCs) that reduces the federal tax rate from 15% to 9% on the first $500,000 of active business income.

Tax Savings Impact:

- Income: $500,000

- Without SBD (15% rate): $75,000 federal tax

- With SBD (9% rate): $45,000 federal tax

- Annual federal tax savings: $30,000

- Plus provincial SBD reduces provincial tax rate (varies by province)

**Eligibility Requirements:

- Must be CCPC (Canadian-controlled private corporation)

- Must earn “active business income” (NOT passive investment income)

- Must be taxable in Canada

Disqualifying Factors:

- Non-resident control (must be controlled by Canadian residents)

- Publicly traded company (must be private)

- Foreign company (must be Canadian-controlled)

Limit Reductions:

The $500,000 limit is reduced if:

- Taxable capital employed in Canada > $10 million (gradual reduction)

- Taxable capital > $15 million (fully eliminated)

- Adjusted aggregate investment income > $50,000 (gradual reduction)

- Adjusted aggregate investment income > $150,000 (fully eliminated)

- Associated companies share the limit

Example with Reduction:

- CCPC with $500,000 active business income

- Taxable capital: $12 million

- Limit reduction applies (between $10M-$15M)

- Eligible for reduced SBD benefit (not full $500,000)

- Consult accountant for precise calculation

Tax Credit #2: Scientific Research & Experimental Development (SR&ED)

What It Is:

A federal tax credit program that provides 15-35% tax credits on qualifying research and development expenses.

**Credit Rates by Company Type:

- CCPC: 35% on first $4.5 million annually (up to $1.575 million per year)

- Other corporations: 15% on unlimited spending

- Enhanced limit: Increased from $3 million to $4.5 million in 2024

Refundable vs. Non-Refundable:

- CCPC: Credit is refundable (receive cash refund if losses)

- Public companies: Credit is non-refundable (reduces taxes owed)

Eligible SR&ED Expenses:

- Researchers’ salaries (wages/salary cost)

- Technician wages

- Lab materials and supplies

- Software development costs

- Equipment (80% of cost)

- Contracted R&D (80% of cost)

Ineligible Expenses:

- General management salaries

- Office overhead allocation

- Routine product testing

- Routine manufacturing

Example SR&ED Benefit:

- CCPC conducting R&D

- Eligible R&D spending: $2,000,000

- SR&ED credit: $2,000,000 × 35% = $700,000 tax credit

- If CCPC has losses: Receive $700,000 refund

- If CCPC has profits: Reduce taxes owed by $700,000

- Effective cost of R&D: $1,300,000 instead of $2,000,000 (35% discount)

Provincial Enhancements:

- Ontario: Additional 10% on Ontario R&D

- Quebec: Up to 30% additional incentives

- British Columbia: 10% additional

- Other provinces: Vary

Filing Requirement:

- Form T661 + detailed schedules

- File within 18 months of fiscal year-end

- CRA reviews claim thoroughly

- Documentation critical (detailed records of R&D activity)

Part 4: Checklists and Action Items

Home Office Deduction Checklist

Step 1: Verify Eligibility

☐ My home is the principal place of my business

☐ OR I have a dedicated workspace used exclusively for business

☐ OR I regularly meet clients/customers at my home

Step 2: Calculate Percentage

☐ Measure office square footage: _____ sq. ft.

☐ Measure total home square footage: _____ sq. ft.

☐ Calculate percentage: Office ÷ Total = _____ %

Step 3: Gather Home Expenses Documentation

☐ Rent or mortgage statements (if mortgage, identify interest vs. principal)

☐ Utility bills (electricity, gas, water, heating, cooling)

☐ Property tax statements

☐ Home insurance premiums

☐ Maintenance and repair receipts

☐ Internet and telephone bills (if split between business/personal, estimate business portion)

Step 4: Calculate Deduction

☐ Sum all eligible home expenses: $_____

☐ Multiply by office percentage: _____ %

☐ Home office deduction: $_____ × _____ % = $____

Vehicle Expense Deduction Checklist

Step 1: Establish Business Use Percentage

☐ Track mileage for minimum 3 months (or full year)

☐ Record business km: _____

☐ Record personal km: _____

☐ Record total km: _____

☐ Calculate business percentage: Business km ÷ Total km = _____%

Step 2: Gather All Vehicle Expense Receipts

☐ Fuel receipts (gas, diesel, propane)

☐ Oil and maintenance receipts

☐ Insurance premium statements

☐ Repair and maintenance invoices

☐ License and registration documentation

☐ Lease or loan interest statements

☐ Parking receipts

Step 3: Sum Total Vehicle Expenses

☐ Total fuel costs: $_____

☐ Total maintenance: $_____

☐ Total insurance: $_____

☐ Total other expenses: $_____

☐ Total annual vehicle expenses: $_____

Step 4: Calculate Deduction

☐ Total expenses × Business percentage = Deductible amount

☐ Example: $6,000 × 75% = $4,500

☐ Total vehicle deduction: $_____

Meals and Entertainment Checklist

Step 1: Gather All Receipts

☐ Client lunch receipts

☐ Entertainment tickets (sporting events, concerts, etc.)

☐ Business dinner receipts

☐ Convention or conference meal receipts

☐ All receipts include date, location, amount, and business purpose

Step 2: Categorize by 50% vs. 100%

50% Rule Applies (Half deductible):

☐ Regular client meals

☐ Business dinners

☐ Entertainment events

100% Exception (Full deductible):

☐ Meals billed to and reimbursed by client

☐ Meals during business travel (primary purpose business)

☐ Incidental refreshments at conventions

☐ If you’re in food/hospitality industry

Step 3: Calculate Deduction

☐ 50% rule expenses: $_____ × 50% = $_____

☐ 100% exception expenses: $_____ × 100% = $_____

☐ Total meals and entertainment deduction: $_____

Part 5: 2026 Planning Opportunities

Opportunity #1: Accelerated Investment Incentive (AII)

What It Is:

100% immediate write-off (first-year expense) for eligible capital property instead of depreciating over multiple years.

Eligible Property:

- Class 44 assets

- Class 46 assets

- Class 50 assets

Timing Window:

- Acquired after April 16, 2024

- Must be available for use before January 1, 2027

- Limited time benefit—expires January 1, 2027

Tax Planning Opportunity:

If you’re considering equipment or technology purchases, buying in 2026 and claiming full deduction in 2026 is more favorable than normal depreciation over 4-8 years.

Opportunity #2: SR&ED Program Expansion for R&D Intensive Businesses

Enhanced CCPC Benefit:

- Limit increased from $3M to $4.5M eligible spending

- 35% credit on first $4.5M (vs. $3M previously)

- Additional $1.5M in spending now qualifies for 35% rate

If Your Business Does R&D:

- Map out all qualifying R&D activities

- Document researcher time and materials

- File SR&ED claim (Form T661)

- Potential for significant cash refunds/tax reductions

Opportunity #3: Small Business Deduction Tax Planning

For Incorporated Businesses:

Ensure you’re structured to maximize SBD:

- Confirm your corporation qualifies as CCPC

- Verify you’re earning active business income (not passive)

- Monitor taxable capital (stays below $10M if possible)

- Monitor investment income (keep below $50K if possible)

- Claim full SBD on first $500,000 of active income

Tax Rate Difference:

- General rate (15%) vs. SBD rate (9%) = 6% difference

- On $500,000 income = $30,000 federal annual savings

- Over 10 years = $300,000 tax savings

Part 6: CRA Compliance Best Practices

Documentation Standards for Home Office

What CRA Expects:

- Detailed home expense documentation (utilities, insurance, rent, property tax, maintenance)

- Square footage measurements (office and home)

- Written calculation of percentage

- Clear business purpose for home office

Common Audit Triggers:

- Home office deduction exceeds 30% of home expenses (seems excessive)

- No documentation for percentage calculation

- Claiming expenses not properly allocated

Avoid:

- Claiming personal expenses mixed with business

- Over-estimating office square footage

- Claiming expenses from shared spaces

Documentation Standards for Vehicle

What CRA Expects:

- Mileage log with dates, destinations, purposes, and odometer readings

- All vehicle expense receipts

- Clear documentation of business vs. personal use

- Logbook method or simplified method documentation

Common Audit Triggers:

- Round-number km claims (3,000 km per month, every month—looks fabricated)

- No mileage documentation

- Claiming commuting to office as business use

- Personal vehicle use exceeding business use

Avoid:

- Estimating mileage from memory

- Failing to differentiate business from personal use

- Claiming family trips as business use

Documentation Standards for Meals & Entertainment

What CRA Expects:

- Dated receipts showing amount, location, attendees, business purpose

- Differentiation between 50% and 100% expenses

- Reasonable amounts (not lavish spending)

- Clear business connection

Common Audit Triggers:

- Claiming 100% of all meals (50% rule applies to most)

- Excessive meal costs

- No business purpose documented

- Vague receipt descriptions

Avoid:

- Claiming personal meals as business meals

- Mixing personal and business entertainment

- Insufficient documentation

Conclusion: Maximizing Deductions While Staying Compliant

Canadian small business owners leave thousands in deductions unclaimed annually—simply because they’re unaware of eligibility rules or intimidated by documentation requirements.

The path to maximum legitimate deductions is straightforward:

- Understand your deductions: Know which expenses are deductible (and which aren’t)

- Calculate correctly: Use proper formulas for home office (%) and vehicle (business km ÷ total km)

- Document meticulously: Keep receipts, logs, and records—this is non-negotiable

- Claim confidently: File deductions supported by documentation

- Consider tax credits: For incorporated businesses, maximize SBD and SR&ED

For CCPC owners, tax credits provide even greater benefits—a $700,000 SR&ED credit can effectively reduce R&D costs by one-third.

The investment in proper documentation and accounting is minimal compared to the tax savings achieved. Most small business owners will save $3,000-$10,000+ annually by properly claiming all eligible deductions.

File with confidence, knowing you’re claiming every dollar legally allowed under Canadian tax law.

Article created for BOMCAS Canada. For tax deduction planning and small business accounting, contact info@bomcas.ca or consult your accountant.

View Our Location

View Our Location

181 Meadowview Bay, Sherwood Park, AB T8H 1P7, Canada (Online Clients Only)

181 Meadowview Bay, Sherwood Park, AB T8H 1P7, Canada (Online Clients Only)