Executive Summary

Green business initiatives are no longer just an environmental responsibility—they’re a financial strategy. In 2025-2026, the Canadian government is offering unprecedented financial incentives for businesses that invest in sustainable technologies, from solar panels to electric vehicles to carbon capture equipment. The total available funding exceeds $93 billion through federal tax credits alone, with additional grants, rebates, and loans available through provincial programs.

For business owners, this creates a remarkable opportunity: implement sustainability improvements your business needs anyway, and let government incentives cover a significant portion of the cost. A company investing $500,000 in renewable energy equipment could claim a $150,000 tax credit. A manufacturer purchasing zero-emission vehicles can write off 100% of the vehicle cost in the first year. A facility installing energy-efficient retrofits can receive 50% of costs back as grants and tax credits.

Yet most Canadian businesses are leaving this money on the table. Many are unaware of available programs. Others think the incentives are too complicated or only apply to large corporations. Some assume their industry doesn’t qualify. In reality, green tax incentives span virtually every business type and operation—from small service companies to major manufacturers, from office buildings to industrial facilities.

This comprehensive guide outlines the six major categories of federal green tax credits, provincial and territorial incentive programs, and practical strategies for maximizing savings while building a sustainable business. By understanding these incentives, you can reduce the true cost of green initiatives by 30-75%, creating a compelling business case for sustainability that simultaneously reduces environmental impact and improves your bottom line.

Part 1: The Canadian Green Tax Incentive Landscape

The $93 Billion Opportunity (2024-2035)

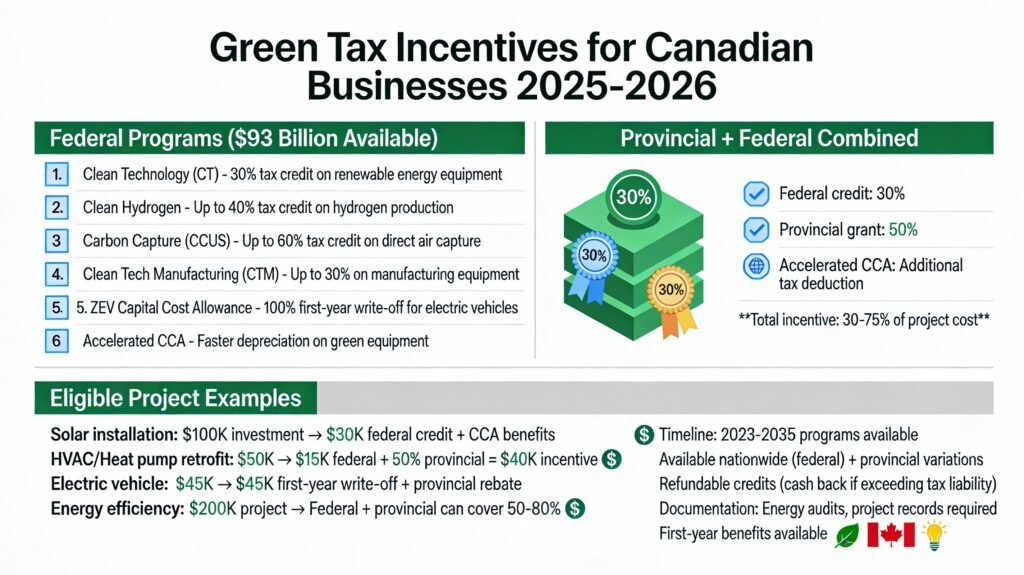

In March 2023, the Canadian federal government announced the Clean Economy Investment Tax Credits (ITCs) program—a $93 billion commitment spanning 2024 through 2035 to support business investment in clean technologies. This represents the largest single climate finance commitment in Canadian history.

The program is structured as a series of refundable tax credits—meaning businesses don’t just reduce their tax liability; if the credit exceeds taxes owed, the government refunds the difference. This is critical: a refundable credit is worth significantly more than a non-refundable credit because it provides cash back to businesses.

Why the government is doing this:

- Net zero by 2050 commitment (legislated)

- Industrial competitiveness: competing with US Inflation Reduction Act ($369B clean energy program)

- Job creation in clean technology sector

- Domestic manufacturing of clean tech equipment

- Greenhouse gas reduction targets

Who benefits:

- Manufacturers of clean energy equipment

- Businesses investing in renewable energy

- Companies decarbonizing operations

- Organizations capturing and using carbon

- Producers of hydrogen and critical minerals

- Vehicle fleets converting to zero-emissions

Federal vs. Provincial Programs: Understanding Your Options

Canadian green incentives operate on both federal and provincial levels. Federal programs (administered by CRA and Natural Resources Canada) are available nationwide. Provincial programs vary significantly by province and are often more generous for businesses located within that province.

Federal programs provide:

- Clean Technology (CT) Investment Tax Credit: 30% on renewable energy and heat recovery equipment

- Clean Hydrogen Investment Tax Credit: Up to 40% on hydrogen production equipment

- Carbon Capture, Utilization & Storage (CCUS) ITC: Up to 60% on direct air capture, 37.5% on transport/storage

- Clean Technology Manufacturing (CTM) ITC: Up to 30% on manufacturing equipment for clean tech products

- Accelerated Capital Cost Allowance (CCA): Faster depreciation on green equipment

- Various grant programs (non-repayable funding) through Natural Resources Canada and other departments

Provincial programs include:

- Ontario: Save on Energy Retrofit Program (50% of retrofit costs)

- BC: CleanBC programs for retrofits and EVs

- Quebec: Green energy incentives and building retrofit programs

- Other provinces: Varying programs for retrofits, renewable energy, and transportation

- Most provinces also administer Canada’s Greener Homes Initiative grants

Strategic approach: Most businesses can stack federal and provincial incentives. A retrofit project might receive 30% from federal tax credits plus 50% from provincial grants, reducing your true cost dramatically. Understanding what’s available in your province is essential.

Part 2: The Six Major Federal Green Tax Credit Programs

1. Clean Technology (CT) Investment Tax Credit—30% Refundable Credit

Rate: 30% refundable tax credit on capital expenditures

Eligible equipment:

- Solar photovoltaic systems

- Wind turbines

- Hydroelectric equipment (small scale)

- Geothermal heating systems

- Energy storage systems (batteries)

- Heat recovery systems

- Biogas and biomass systems

How it works:

- Make a capital investment in eligible equipment

- Claim the 30% credit on your tax return

- If the credit exceeds taxes owed, CRA refunds the difference

- Example: $100,000 solar installation = $30,000 tax credit

Available period: March 28, 2023 through December 31, 2033 (10+ years of program availability)

Key requirements:

- Equipment must be used in Canada

- Equipment must be new (not used)

- Located in Canada

- Proper documentation of purchase and installation

Combined with accelerated CCA: You can claim both the 30% tax credit AND use accelerated depreciation for the remaining 70% of the cost. This creates significant tax benefits in the year of installation.

Real-world example:

A manufacturing facility invests $500,000 in solar panels:

- 30% CT ITC: $150,000 (tax credit)

- Remaining cost basis: $350,000

- CCA depreciation: $350,000 at 30% declining balance = $105,000 Year 1 deduction

- Total Year 1 tax benefit: $255,000 (on $500,000 investment)

- This dramatically reduces the effective cost

2. Clean Hydrogen Investment Tax Credit—Up to 40% Refundable Credit

Rate: Up to 40% refundable tax credit (conditions apply)

Eligible projects:

- Electrolysis equipment for hydrogen production (zero-carbon hydrogen)

- Natural gas reforming with CCUS (carbon capture on hydrogen production)

- Clean ammonia production (15% credit)

- Equipment manufacturing for hydrogen industry

Why it matters: Hydrogen is emerging as critical for decarbonizing heavy industry, transportation, and energy. The government is incentivizing domestic hydrogen production.

Rate structure:

- Hydrogen from electrolysis: Up to 40% credit

- Ammonia from electrolysis: 15% credit

- Conditions-based reductions: Credits can be 30% or 20% depending on project size, wage requirements, and other conditions

Timeline: March 28, 2023 through December 31, 2033

Application process:

- More complex than CT credit

- Requires pre-project notification to Natural Resources Canada

- Technical and financial documentation required

- Non-binding feedback before investment

Who should consider this: Primarily large industrial operators in petrochemicals, mining, steel, and emerging hydrogen production companies. Less relevant for typical SMBs unless involved in hydrogen production or use.

3. Carbon Capture, Utilization & Storage (CCUS) Investment Tax Credit—Up to 60%

Rate: Up to 60% refundable tax credit (direct air capture); 37.5% for transport/storage/use

Eligible activities:

- Direct air capture (DAC): Removing CO₂ directly from atmosphere—60% credit

- Carbon transportation: Moving captured carbon—37.5% credit

- Carbon storage: Geological storage—37.5% credit

- Carbon utilization: Using captured carbon in products—37.5% credit

2025 Budget Update: The federal government extended the CCUS ITC from 2030 to 2035, confirming long-term commitment. After 2035, rates decrease (30%, 25%, 18.75% in subsequent years).

Project requirements:

- 20-year minimum capture/storage period

- Detailed project plan required

- Initial technical and financial evaluation

- Annual reporting on capture volumes

- Independent audits

Capital eligible: Equipment, buildings, and infrastructure for CCUS operations

Why the high rate: Direct air capture is expensive and emerging technology. The 60% credit aims to make these projects financially viable while climate impact scales globally.

Who benefits:

- Large industrial emitters (oil, gas, steel, cement)

- Emerging carbon removal technology companies

- Industrial users of CO₂ (beverages, chemicals, food)

- Less common for typical SMBs but important for specific industries

4. Clean Technology Manufacturing (CTM) Investment Tax Credit—Up to 30%

Rate: Up to 30% refundable tax credit on eligible property

Eligible equipment:

- Machinery for manufacturing renewable energy equipment (solar panels, wind turbines, batteries)

- Machinery for manufacturing zero-emission vehicles (EVs)

- Machinery for manufacturing electrical energy storage systems

- Critical minerals processing equipment

2025 Budget expansion: The government expanded CTM to include five additional critical minerals:

- Antimony, indium, gallium, germanium, scandium

- Reflects battery and clean tech equipment manufacturing expansion

Timeline: Property must be available for use 2024-2031 (eligible period for claiming credit)

Credit phases:

- 2024-2029: 30% credit

- 2030-2031: 24% credit

Why it matters: The government is trying to establish Canadian manufacturing capacity for clean tech equipment, rather than importing everything. Businesses building factories to produce batteries, solar panels, EVs, or electric motors can claim significant credits.

Application requirements:

- Pre-project notification to Natural Resources Canada

- Technical documentation of manufacturing process

- Proof the equipment is for eligible manufacturing

- Annual verification and reporting

5. Capital Cost Allowance (CCA) Acceleration for Green Equipment

What it is: Faster depreciation write-offs for renewable energy and energy-efficient equipment

Standard CCA classes for green equipment:

- Class 43.1: 30% declining balance (renewable energy, energy recovery, alternative fuel engines)

- Class 43.2: 50% declining balance (additional renewable energy equipment, air/ground source heat pumps)

Example of accelerated benefit:

A business invests $100,000 in air-source heat pump equipment (Class 43.2):

- Year 1: $50,000 CCA deduction (50% of cost)

- Year 2: $25,000 deduction (50% of remaining $50,000)

- Year 3: $12,500 deduction

- Rapid write-off vs. standard 20-25% rates

Combined with tax credits: You can claim BOTH the accelerated CCA AND the Clean Technology tax credit, creating powerful combined benefits

No application required: Unlike the more complex credits, CCA acceleration is automatically available—just claim on your tax return.

Eligible equipment:

- Solar panels and systems

- Wind turbines

- Geothermal systems

- Heat pumps

- Energy recovery systems

- Biogas/biomass systems

- Batteries and energy storage

Part 3: Provincial & Territorial Green Incentives

While federal credits provide a base level of support nationwide, most provinces offer additional programs that can dramatically increase total incentive value. These vary significantly by province.

Ontario: Save on Energy Retrofit Program

Coverage: Covers 50% of eligible retrofit project costs (varies by stream)

Eligible projects:

- HVAC system upgrades

- Building automation systems

- Boiler replacements

- Heat pump installations

- Lighting upgrades

- Industrial energy efficiency measures

Two streams:

- Prescriptive: Standard incentive amounts for common retrofits

- Custom: Tailored to your specific project, up to $0.20/kWh energy savings

Maximum incentive: Typically $100,000-$250,000 per project (higher for large industrial facilities)

Double incentives: Eligible communities/regions can receive double incentives (up to 50% of costs)

Industrial advantage: Energy Management Information System (EMIS) grants: $50,000-$250,000 depending on annual energy consumption

Application: First-come, first-served; apply through Enbridge or natural gas provider

British Columbia: CleanBC Programs

CleanBC Home Retrofit Rebate:

- Heat pump rebates: $5,000-$10,000 depending on efficiency

- Insulation and air sealing: Up to $1,000

- Windows and doors: Up to $1,000

- Water heating: Up to $2,500

- Home energy audit: Up to $400

CleanBC EV Incentive (commercial/fleet):

- Grants available for zero-emission vehicle purchases (business vehicles)

- Income-tiered for individuals and organizations

- Stackable with federal incentives

Quebec: Green Energy Programs

Energy Efficiency Grants:

- Building envelope improvements

- HVAC system upgrades

- Renewable energy systems

- Typical grant: 20-50% of eligible costs

EV Incentive (currently declining):

- $4,000 (2025), reducing to $2,000 (2026), ending 2027

- Available for personal and commercial vehicles

Canada Greener Homes Initiative (Nationwide)

Federal grants for residential retrofits (available through provincial partners):

Grant amounts:

- Energy audit: $600 rebate

- Heat pump installation: $2,500 (mini-split), $3,000-$5,000 (ground-source)

- Heat pump water heater: $1,200-$2,000

- Solar PV system: $1,000 per kW (minimum 1.0 kW)

- Insulation and air sealing: $200-$800

- Window replacement: $400-$800

- Oil-to-heat-pump conversion: Special affordability program

Loans available: Up to $40,000 interest-free for retrofits

Process:

- Get energy audit ($600 rebate available)

- Identify retrofit improvements

- Claim grant amounts

- Arrange financing if needed

Part 4: Zero-Emission Vehicle (ZEV) Tax Incentives

For businesses and fleets, zero-emission vehicles combine purchase incentives with exceptional tax benefits.

Capital Cost Allowance for Business ZEVs—100% First-Year Write-Off

What it is: A special CCA rule allowing businesses to write off 100% of a ZEV purchase cost in the year of acquisition (up to approximately $55,000 vehicle cost threshold, with some variation).

Comparison:

- Traditional vehicle: CCA write-off over multiple years (typically 15-20% per year)

- Zero-emission vehicle: 100% write-off in Year 1

Tax benefit example:

A small business purchases a $45,000 electric van:

- Traditional vehicle: $6,750 Year 1 CCA deduction (15%)

- ZEV: $45,000 Year 1 deduction (100%)

- Tax savings: $45,000 × 26.5% (marginal rate) = $11,925 Year 1

Eligibility:

- Passenger vehicles (typically <15,000 kg GVWR)

- Light-duty trucks

- Medium-duty zero-emission vehicles

- Motorcycles and scooters (some provinces)

Not eligible:

- Vehicles over weight threshold

- Imported used vehicles (some restrictions)

- Personal-use vehicles (business-use only)

Stacks with purchase incentives: You can claim the ZEV tax write-off in the same year as federal/provincial purchase rebates.

Federal iZEV Purchase Incentive (Status: Paused Jan 2025)

Program status: The federal purchase incentive was paused in January 2025 and was scheduled to expire March 31, 2025. As of 2026, federal purchase rebates are not active.

Previous program details (for context):

- $5,000 rebate for passenger vehicles

- Only vehicles made in Canada or meeting free trade requirements

- Income limits applied

Current status: Businesses should focus on provincial rebates and tax deductions.

Provincial ZEV Purchase Incentives (Vary by Province)

BC CleanBC EV Incentive:

- Up to $4,000 for qualifying vehicles

- Income-tiered (lower income = higher rebate)

- MSRP threshold around $50,000

- Stackable with CCA write-off

Quebec:

- $4,000 (2025), decreasing to $2,000 (2026), ending 2027

- Available for personal and commercial vehicles

- Some restrictions on vehicle cost

Newfoundland & Labrador:

- $2,500 rebate

- Newly expanded to include used EVs

- Businesses and individuals eligible

Other provinces: Vary; check your provincial government website for current programs.

Medium/Heavy-Duty ZEV Program (iMHZEV)

For: Larger commercial vehicles (trucks, buses, delivery vehicles)

Incentive: Up to $200,000 per vehicle for eligible medium/heavy-duty zero-emission vehicles

Eligible vehicles:

- Class 6-8 medium/heavy-duty trucks

- Transit buses

- Delivery vehicles

- Refuse trucks

Eligibility requirements:

- Canadian business with registered Canadian office

- Vehicles used for commercial purposes in Canada

- Non-competitive basis; ongoing program

Examples of eligible vehicles:

- Tesla Semi (when available for delivery)

- Electric delivery trucks (Freightliner, Volvo, etc.)

- Electric buses

- Electric garbage trucks

- Hybrid-electric large vehicles (often eligible)

Application process:

- Application through supplier/dealer

- Non-competitive; first-come, first-served

- Vehicle must be delivered within specified timeframe

Combined incentive potential: A company purchasing electric delivery trucks could receive $200,000 per vehicle PLUS potential provincial incentives in some provinces, creating substantial cost reduction.

Part 5: Practical Strategies to Maximize Your Green Incentives

Strategy 1: Comprehensive Energy Audit First

Step 1: Conduct a professional energy audit (government partially subsidizes: $600 rebate available).

Why it matters:

- Identifies all eligible retrofit opportunities

- Prioritizes improvements by cost and savings

- Documentation supports grant applications

- Creates baseline for measuring energy savings

Output: A report showing potential savings and eligible improvements, helping you identify which retrofits qualify for incentives.

Strategy 2: Stack Federal + Provincial + Accelerated Depreciation

Example: $200,000 HVAC + Heat Pump Retrofit in Ontario

- Federal Clean Technology credit (30%): $60,000

- Ontario Save on Energy (50%): $100,000

- Accelerated CCA (Year 1): $40,000 deduction = $10,600 tax savings (26.5% rate)

- Total incentive value: $170,600 on $200,000 project

- True cost to business: $29,400 (15% of investment)

Strategy 3: Timing & Phasing

Consider multi-year phasing:

- Large projects can be split across years

- Spreads capital costs

- May access both current and future grant programs

- Ensures you have sufficient taxable income to use credits

Example: Plan $500,000 solar installation across 2026-2027:

- Year 1 ($250K): Receive $75K credit + accelerated CCA

- Year 2 ($250K): Receive $75K credit + accelerated CCA + potential new programs

Strategy 4: Document Everything

Critical for claiming incentives:

- Purchase invoices and contracts

- Installation records and certifications

- Equipment specifications (must match eligible criteria)

- Professional energy audit reports

- Financial records of total project cost

- Timeline and completion dates

6-year retention: Keep all documentation for 6 years in case of CRA audit.

Strategy 5: Professional Guidance

When to engage experts:

- Project cost exceeds $50,000

- Claiming Clean Hydrogen or CCUS credits (complex)

- Multi-year phasing strategy

- Manufacturing or industrial projects

- Multi-location or multi-province operations

Professional services available:

- Accountants: Tax credit planning, optimization

- Energy consultants: Retrofit design, efficiency analysis

- Environmental consultants: Carbon reduction strategy

- Government liaison specialists: Grant applications

Strategy 6: ESG & Sustainability Reporting

Green incentives support ESG strategy:

- Document carbon reductions from projects

- Track energy savings and cost reductions

- Create sustainability reports for stakeholders

- Potential for employee engagement and recruitment

- Marketing value: “Certified sustainable business”

- Investor appeal (growing ESG focus)

Part 6: 2025-2026 Regulatory & Budget Updates

Clean Electricity Regulations

The federal government is advancing regulations requiring clean electricity by 2035 and net-zero by 2050. This creates urgency for businesses to invest in clean energy—particularly for industrial facilities.

Implications for businesses:

- Industrial customers will face pressure to decarbonize

- Electricity prices may increase for carbon-intensive grids

- Early investment in renewable energy locks in lower long-term costs

- Clean equipment manufacturers benefit from increased demand

Extended CCUS Investment Tax Credit Timeline

The 2025 Budget confirmed the CCUS ITC will continue through 2035 (extended 5 years from previous 2030 end date), with phased rate reductions:

- 2022-2035: Full rates (60%, 37.5%)

- 2036-2040: Declining rates (30%, 25%, 18.75%)

Impact: Long-term confidence for CCUS project development; rate urgency decreases.

Manufacturing and Processing Expansion

The Clean Technology Manufacturing credit has been expanded to include critical minerals processing—reflecting Canada’s strategic focus on securing supply chains for batteries, electronics, and clean tech equipment.

Pay Equity and Wage Requirements

Some credits (hydrogen, manufacturing) include conditions based on average wages paid. Budget 2025 continues to include these workforce development requirements.

Part 7: Action Plan—Get Started Today

30-Day Plan

Week 1:

- Audit current energy consumption and carbon footprint

- Identify green initiatives your business needs (HVAC, lighting, EV, insulation, etc.)

- Research federal programs relevant to your industry

- Check provincial programs for your region

Week 2:

- Book a professional energy audit ($600 rebate available)

- Gather project cost estimates from contractors

- Research equipment that qualifies for Clean Technology credit

Week 3:

- Calculate total incentive value (federal + provincial + CCA)

- Develop preliminary project timeline and phasing

- Consult with accountant on tax credit optimization

Week 4:

- Finalize retrofit/equipment specifications

- Submit grant applications (if applicable)

- Order equipment and schedule installation

90-Day Plan

Target: Have initial project approved, funded, or underway

- Receive energy audit report

- Identify 2-3 priority improvements

- Secure financing (grants + loans + own capital)

- Begin equipment procurement

- Document all costs and timelines

Annual Review

Schedule annually (ideally in Q4) to:

- Review new 2027 programs and rates

- Plan next year’s green initiatives

- Calculate energy savings from 2025-2026 projects

- Update ESG/sustainability reporting

- File tax credits and claims with accountant

Conclusion: Green Is Profitable

The combination of federal and provincial green tax incentives has fundamentally changed the economics of sustainability. Investments that once required multi-year paybacks now break even in 2-4 years thanks to government support. Projects that were marginal on pure ROI are now clearly justified.

For business owners and financial leaders, the opportunity is clear: green initiatives are no longer an expense center or CSR checkbox—they’re a profit center. By understanding and leveraging available incentives, you reduce the true cost of necessary sustainability investments by 30-75%, improve operational efficiency, reduce energy costs, strengthen employee recruitment and retention, and build long-term competitive advantage.

The $93 billion federal commitment runs through 2035. Provincial programs are expanding. The urgency from climate regulations is increasing. The time to act is now, while incentive rates are at their maximum and funding is most available.

Your next step: schedule an energy audit (government partially subsidizes) and identify your first green initiative. The financial incentives available are substantial—and they won’t last forever.

Article created for BOMCAS Canada, Edmonton & Sherwood Park. For questions about green business tax incentives, sustainability planning, or green initiative financing, contact info@bomcas.ca or 780-667-5250.

View Our Location

View Our Location

181 Meadowview Bay, Sherwood Park, AB T8H 1P7, Canada (Online Clients Only)

181 Meadowview Bay, Sherwood Park, AB T8H 1P7, Canada (Online Clients Only)